Economy

Vision for the future monetary system

The future monetary system should meld new technological capabilities with a superior representation of central bank money at its core. Rooted in trust in the currency, the advantages of new digital technologies can thus be reaped through interoperability and network effects. This allows new payment systems to scale and serve the real economy. The system can thus adapt to new demands as they arise – while ensuring the singleness of money across new and innovative activities.

Central banks are uniquely positioned to provide the core of the future monetary system, as one of their fundamental roles is to issue central bank money (M0), which serves as the unit of account in the economy. From the basic promise embodied in the unit of account, all other promises in the economy follow.

The second fundamental role of the central bank, building on the first, is to provide the means for the ultimate finality of payments by using its balance sheet. The central bank is the trusted intermediary that debits the account of the ultimate payer and credits the account of the ultimate payee. Once the accounts are debited and credited in this way, the payment is final and irrevocable.

The third role of the central bank is to support the smooth functioning of the payment system by providing sufficient liquidity for settlement. Such liquidity provision ensures that no logjams will impede the workings of the payment system when a payment is delayed because the sender is waiting for incoming funds.

The fourth role of the central bank is to safeguard the integrity of the payment system through regulation, supervision and oversight. Many central banks also have a role in supervising and regulating commercial banks and other core participants of the payment system. These intertwined functions of the central bank leave it well placed to provide the foundation for innovative private sector services.24

The future monetary system builds on these roles of the central bank to give full scope for new capabilities of central bank money and innovative services built on top of them. New private applications will be able to run not on stablecoins, but on superior technological representations of M0 – such as wholesale and retail CBDCs, and through retail FPS that settle on the central bank balance sheet. Central bank innovations can thereby support a wide range of new activities. Because central banks are mandated to serve the public interest, they can design public infrastructures to support the monetary system’s high-level policy goals (Table 1, final column) from the ground up.

This vision entails a number of components that require both formal definitions and examples. The section first introduces and explains these components. It next gives a metaphor for what the future system will look like, both domestically and across borders. Finally, it dives into the specifics of reforms to central bank money at the wholesale, retail and cross-border level, before reviewing where central banks stand in achieving this vision.

Components of the future monetary system

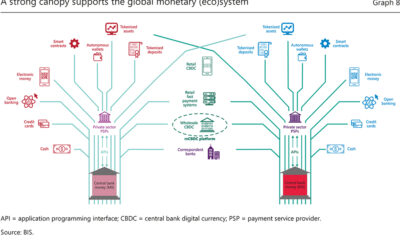

The future monetary system builds on the tried and trusted division of roles between the central bank – which provides the foundations of the system – and private sector entities that conduct the customer-facing activities. On top of this traditional division of labour come new standards such as application programming interfaces (APIs, see glossary) that greatly enhance the interoperability of services and associated network effects. Not least are new technical capabilities encompassing programmability, composability and tokenisation, which have so far been associated with the crypto universe.

This vision contains components at both the wholesale and retail level, which enable a number of new features (in bold).

At the wholesale level, central bank digital currencies (CBDCs) can offer new capabilities and enable transactions between financial intermediaries that go beyond the traditional medium of central bank reserves. Wholesale CBDCs that are transacted using permissioned distributed ledger technology (DLT) offer programmability and atomic settlement, so that transactions are executed automatically when set conditions are met. They allow a number of different functions to be combined and executed together, thus facilitating the composability of transactions. These new capabilities not only permit the expansion of the types of transactions, but also enable transactions between a much wider range of financial intermediaries – not just commercial banks. Wholesale CBDCs also work together across borders, through multi-CBDC arrangements involving multiple central banks and currencies.

Within the new functions unlocked by wholesale CBDCs, one set of applications deserves special mention – namely, those stemming from the tokenisation of deposits (M1), and other forms of money that are represented on permissioned DLT networks.25 The role of intermediaries in settling transactions was one of the major advances in the history of money, tracing back to the role of public deposit banks in Europe in the early history of central banking.26 Bank deposits serve as the payment medium, as the intermediary debits the account of the payer and credits the account of the receiver. The tokenisation of deposits takes this principle and translates the operation to DLT by creating a digital representation of deposits on the DLT platform, and settling them in a decentralised manner. This could facilitate new forms of exchange, including fractional ownership of securities and real assets, allowing for innovative financial services that extend well beyond payments.

At the customer-facing, or “retail” level, the enhanced capabilities of the financial intermediaries benefit users in the form of improved interoperability between customer-facing platforms provided by intermediaries. Core to this interoperability are APIs, through which users of one platform can easily communicate and send instructions to other, interlinked platforms. This way, innovations at the retail level promote greater competition, lower costs and expanded financial inclusion.

Concretely, retail FPS and retail CBDCs constitute another core feature of the future monetary system. Retail FPS are systems in which the transmission of a payment message and the availability of final funds to the payee occur in (near) real time, on or as near to 24/7 as possible. Many are operated by the central bank. Retail CBDCs are a type of CBDC that is directly accessible by households and businesses. Both retail CBDCs and FPS allow for instant payments between end users, through a range of interfaces and competing private PSPs. They hence build on the two-tiered system of the central bank and private PSPs. Retail CBDCs and FPS share a number of further key features and can thus be seen as lying on a continuum. Both are supported by a data architecture with digital identification and APIs that enable secure data exchange, thus supporting greater user control over financial data. By providing an open platform, they promote efficiency and greater competition between private sector PSPs, thus facilitating lower costs in payment services. Through inclusive design features, both can support financial inclusion for users that currently do not have access to digital payments.

Details of the wholesale and retail components are expanded upon below. For each of these, an advanced representation of central bank money supports private sector services that serve the real economy. The central bank supports the singleness of the currency, and interoperability – the ability of participants to transact in different systems without having to participate in each.27 This allows network effects to take hold, whereby the use of a service by one party makes it more attractive for others.

Source: bis.org